Many trucks in transit are / were stuck during lockdown. Some insured have already taken care of them, while some are yet to take care. Some areas are accessible, some yet under lockdown, and, lockdown in any area can occur overnight. So what is the scenario here? What is required from the assured? This article will try to answer some of the queries.

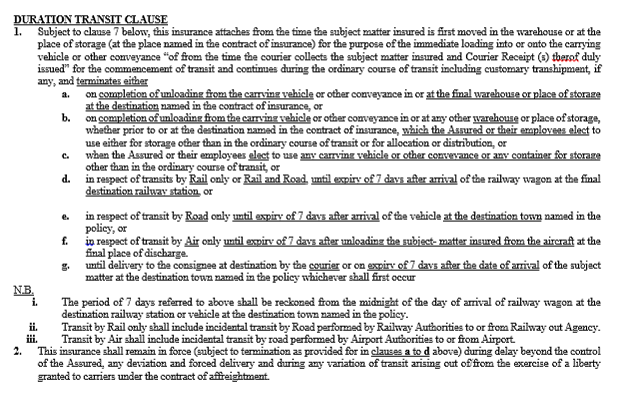

The all-risk marine cargo policy in all forms when operational for inland transit is governed by “Duration Transit Clause”. The delays are otherwise excluded and no insurers cover them. However due to the above clause, some relief is there. This clause reads as under:

So, Interpretation is as under for lockdown period (ie. delay beyond the control of the assured):

- If the cargo movement is by rail or rail + road then cover ends after 7 days of the arrival at the destination rail head.

- If the cargo movement is by road and the truck is stuck enroute and cannot reach its final warehouse then following can happen:

- The material is unloaded enroute and stored in intermediate warehouse.

- Effect: The cover ends almost immediately at the time of unloading.

- Required action: Take cover for intermediate storage.

- The material is taken by alternate modes to the final warehouse, say, 200 bags in single truck are arranged in 10 bag per rickshaw to the final warehouse.

- Effect: The cover ends after arrival at the final warehouse.

- The material is left in the truck and the truck is stranded somewhere, but is in the safe custody of the carrier. The carrier is waiting for the final delivery at the final warehouse.

- Effect: The coverage is automatically extended upto the time the material reaches its destination.

- Required Action: Ensure the cargo is safe in the hands of the carrier. This is the duty of the assured. The assured has to act as if uninsured and take care of the material in most prudent manner. Ensure as under:

- The material is unloaded enroute and stored in intermediate warehouse.

- The location of the truck layover is known to the assured.

- If possible, keep own person posted at the location of layover.

- Ensure that the material is under lock and key and tightly packed tarpaulins.

- In case of any mishap, assured should coordinate with the carriers and local authorities and help salvage the situation by active participation.

- Lodge insurance claim without delay.

- In case, assured cannot contact insurers, services of IRDA licenced surveyors to arrange survey can be used.

The above situation is specific for the cargos by road, which includes couriers, by hand, by air etc. Cargos moving by rail lose their cover the moment they reach destination station. Hence such cargo need special care and need to be immediately taken to the destination and unloaded either at destination or at some intermediate godown. Such cargo cannot be left at the mercy of the carrier. Such claims are liable to be denied by the insurers.